Contents

Separation challenges 1

1 At a glance 2

1.1 Key facts 2

1.2 Key impacts 3

2 Identifying separate lease components 4

2.1 Combining contracts 4

2.2 Separate lease components 6

2.3 Lessors – Additional considerations for land

and buildings 10

2.4 Portfolio approach 14

3 Identifying non-lease components 16

3.1 Non-lease components 16

3.2 Practical expedient for lessees – Combining

lease and non-lease components 20

4 Allocating the consideration 24

4.1 Contract consideration 24

4.2 Allocation of consideration 26

4.3 Lessor allocation 27

4.4 Lessee allocation 32

4.5 Allocation of variable consideration 37

5 Reallocating the consideration 41

5.1 Modification of contracts 41

5.2 Remeasurement of lease payments 45

Appendix I – IFRS 16 at a glance 52

Appendix II – List of examples 53

About this publication 55

Keeping in touch 56

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Separation challenges

Lease agreements frequently bundle multiple components – from complex

outsourcing arrangements, to simple real estate leases in which the landlord

provides building maintenance. If your business has leases, you will probably face

component questions when implementing IFRS 16 Leases.

The lease component is the unit of account for lease accounting. Lessors and

lessees need to identify, and generally separate, lease and non-lease components

to apply the new standard. To do this, they need to allocate the consideration in the

contract between the components that they account for separately.

For a lessor, this process is necessary to correctly distinguish lease income from

other revenue. Lessors generally apply IFRS 15 Revenue from Contracts with

Customers to do this.

For a lessee, this process has a more fundamental accounting impact – it

determines what proportion of a contract will be recognised on-balance sheet. The

new standard has specific guidance on how to determine this.

This publication contains practical guidance and examples showing how to

identify lease and non-lease components in a contract and how to allocate the

consideration. We hope you will find it useful as you apply the new standard.

Kimber Bascom

Ramon Jubels

Sylvie Leger

Brian O’Donovan

KPMG’s global IFRS leases leadership team

KPMG International Standards Group

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 | Lease components

1 At a glance

1.1 Key facts

The lease component is the unit of account for lease accounting.

Lessors and lessees separate lease components from other lease components

and, generally, from non-lease components such as services. They then allocate

– and, if necessary, reallocate – the consideration in the contract between the

components that they account for separately.

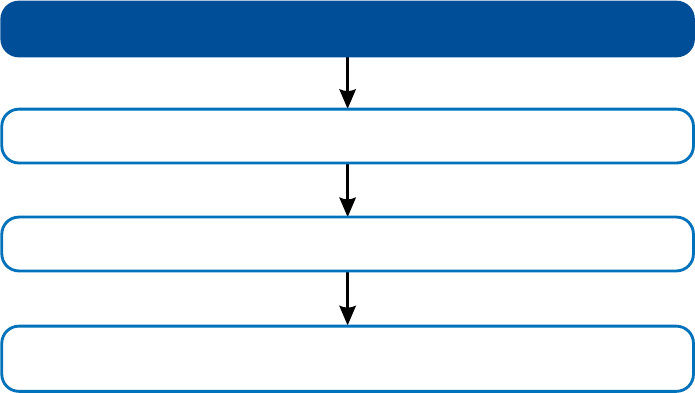

The key steps in accounting for the components of a contract are as follows.

Identify separate lease components (see )Chapter 2

Identify non-lease components (see )Chapter 3

Allocate consideration (see )Chapter 4

Reallocate consideration on lease modification or

reassessment (see )Chapter 5

A lessor applies IFRS 15 to separate components. A lessee applies specific

guidance in the new standard that is similar to, but less detailed than, IFRS 15.

For lessees only, a practical expedient allows a lease and associated non-lease

components to be accounted for as a single lease component rather than

separately (see Section3.2). Otherwise, lease components and non-lease

components are always separated, with non-lease components accounted for

under other standards.

Once the lease and non-lease components have been identified and separated,

the lessee allocates the contract consideration to each lease component on the

basis of its stand-alone price and the aggregate stand-alone prices of the non-

lease components.

All of this is done at the beginning of a contract, so that each lease component

can be accounted for from its commencement date. In addition, if a contract is

modified, or the new standard requires the lease payments to be reassessed, then

subsequent reallocations may be necessary (see Chapter 5).

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1 At a glance | 3

1.2 Key impacts

|

1.2 Key impacts

Distinguishing lease income from other revenue. For lessors, identifying

components and allocating consideration will determine the split of lease income

vs revenue from contracts with customers. These amounts are often presented,

and must be disclosed, separately. For example, a real estate company will need

to distinguish lease income from revenue for other building-related services – e.g.

common area maintenance (CAM).

Determining what proportion of a contract will be on-balance sheet. For

lessees, distinguishing between lease components (generally on-balance sheet)

and non-lease components (generally off-balance sheet) will be a key driver of the

impact of the new standard. This will also require careful allocation of consideration

between components.

Deciding whether to apply the practical expedient. Lessees will need to decide

whether, and if so when, to apply the practical expedient to combine a lease

component with associated non-lease components. This decision must be made

separately for each class of underlying asset. Applying the practical expedient will

generally simplify application of the new standard – but when payments are fixed,

this will increase reported assets and liabilities, and impact many financial ratios.

Identifying components and gathering information. This may require a

substantial effort to identify all components, gather information on the stand-alone

prices and allocate the consideration on commencement, reassessment and

modification of the lease.

New estimates and judgements. The new standard introduces new estimates

and judgements that affect the measurement of lease liabilities. A lessee

determines the liability at commencement and may be required to remeasure it –

e.g. remeasurement of the lease components on a reassessment or modification.

This will require ongoing monitoring and increase financial statement volatility.

Balance sheet volatility. The new standard introduces financial statement

volatility to assets and liabilities for lessees and lessors, due to the requirements

to account for reassessment and lease modifications. This may impact a

company’s ability to accurately predict and forecast results and will require

ongoing monitoring.

Changes in contract terms and business practices. The impact of the new

standard is not limited only to financial reporting. It may prompt changes to

certain contract terms and business practices – e.g. changes in the structuring or

pricing of a lease agreement, including the type of variability of lease payments

and the inclusion of options in the contract. The new standard is likely to

affect departments beyond financial reporting – including treasury, tax, legal,

procurement, real estate, budgeting, sales, internal audit and IT.

New systems and processes. Companies should ensure that they have systems

and processes that enable them to identify separate lease and non-lease components

and gather information for allocating consideration to comply with the requirements.

Careful communication with stakeholders. Investors and other stakeholders will

want to understand the new standard’s impact on the business. Areas of interest

may include the effect on financial position and financial results, the costs of

implementation and any proposed changes to business practices.

Sufficient documentation. The judgements, assumptions and estimates applied

in determining how to measure the lease liability at the commencement date, as

well as remeasurement when a reassessment or modification occurs, will need to

be documented.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 | Lease components

2 Identifying separate

lease components

Each separate lease component is a unit of account to be

accounted for under the new standard.

IFRS 16.12, B2, B32, BC130 When a company concludes that a contract is or contains a lease, it identifies each

separate lease component, which is the unit of account under the new standard.

However, before setting out to identify and separate lease components, it is

important to establish whether the new standard requires you to assess a single

contract or a combination of contracts. Separate accounting for multiple contracts

may not always deliver a faithful representation of the transaction.

2.1 Combining contracts

IFRS 16.B2 It is usually appropriate to account for each contract individually. However, when

two or more contracts are entered into ‘at or near the same time’ with the same

counterparty (or related parties of the counterparty), the contracts are combined as

a single contract if one or more of the following criteria are met:

– the contracts are negotiated as a package with an overall commercial objective

that cannot be understood without considering the contracts together;

– the amount of consideration to be paid in one contract depends on the price or

performance of the other contract(s); or

– the rights to use underlying assets conveyed in the contracts form a single

lease component (see Section 2.2).

Example 1 – Combining contracts

IFRS 16.B2

Lessee S leases a specifically identified space in a building and a printing press

from Lessor L for three years. S enters into two separate contracts, executed

within a few days of each other.

The contractual payments for the building space are fixed at 250,000 per year

and payments for the printing press are based entirely on the level of use – i.e.

75 for each hour operated.

The estimated stand-alone prices of the building space and printing press are

300,000 per year and 50 for each hour operated, respectively.

S and L each predict that the printing press will be operated for 2,000 hours per

year over the three-year lease term.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 5

2.1 Combining contracts

|

S and L conclude that the contracts are combined and considered as a single

contract under the new standard. This is because the two contracts are

executed near the same time with the same counterparty, and together they

fulfil a single commercial objective. L agrees to a lower fixed payment for the

building space contract to incentivise S, with the expectation of making up the

difference with above-market variable payments in the printing press contract.

Example 2 – Contracts combined in a group

IFRS 16.B2

Company P has two divisions – S and T.

S enters into an arrangement with Supplier E for a right to store its gas in a

specified storage tank that has no separate compartments. At inception of the

contract, S has rights to use 50% of the storage tank’s capacity throughout the

term of the contract.

On the same date, T enters into a separate arrangement with E to use 50% of

the capacity of the same storage tank.

Storage tank

Storage rights of Division S

50%

Storage rights of Division T

50%

In this scenario, P concludes that the two contracts are combined and

considered as a single contract, even if the contracts are executed by different

divisions.

Therefore, assuming that the other elements of the lease definition are met, the

arrangement is a lease from P’s perspective. When the two arrangements are

combined, P has rights to use substantially all of the storage tank’s capacity.

How does a company determine whether the contracts were

entered into ‘at or near the same time’?

IFRS 16.BC130

The new standard does not provide any guidance on the meaning of ‘at or near

the same time’. A company considers its customary business practices and

other reasonable expectations – e.g. changes to contracting practices – when

evaluating whether two or more contracts have been entered into at or near

the same time. Additionally, companies evaluate why the arrangements were

written as separate contracts and how the contracts were negotiated – e.g.

both contracts negotiated with the same parties vs different divisions within a

company negotiating separately.

A company considers specific facts and circumstances that may be unusual.

For example, a company could combine two or more large contracts that were

entered into at different times if they were clearly negotiated and discussed

over the same period of time and appear to be significantly inter-related.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

6 | Lease components

How does combining contracts affect lease accounting?

IFRS 16.BC130–BC132

The objective of the requirement to combine contracts is to faithfully represent

the transaction. For example, if two parties enter into a contract for the lease of

an asset for one year starting today and then sign another contract to lease the

same asset starting one year later, it is not appropriate to apply the short-term

lease exemption to these two contracts. For more detail on the application of

short-term lease exemption, see 6.2.2 in our Lease Definition publication.

The requirement’s intention is to limit structuring opportunities to avoid

lease accounting by separating contracts. These would particularly affect the

company’s accounting for sale-and-leaseback transactions, short-term leases

and leases of low-value assets.

If the combined contracts include multiple lease and non-lease components,

then the allocation to the components may differ from those amounts allocated

based on the original, separate contracts.

2.2 Separate lease components

IFRS 16.12, BC133 After identifying that a contract, or a combination of contracts, is or contains a

lease, a company identifies each separate lease component. The guidance on what

constitutes a separate lease component is the same for lessees and lessors.

IFRS 16.B32–B33 A lease contract may allow the lessee the right to use multiple assets – e.g. a

building and equipment. If a lease contract involves the use of multiple assets,

then a company assesses whether the right to use each of these underlying

assets meets the criteria to be identified as a separate lease component. The right

to use an underlying asset is a separate lease component if both of the following

criteria are met:

– the lessee can benefit from using the underlying asset either on its own or

together with other resources that are readily available; and

– the asset is neither highly dependent on, nor highly inter-related with, the other

assets in the contract.

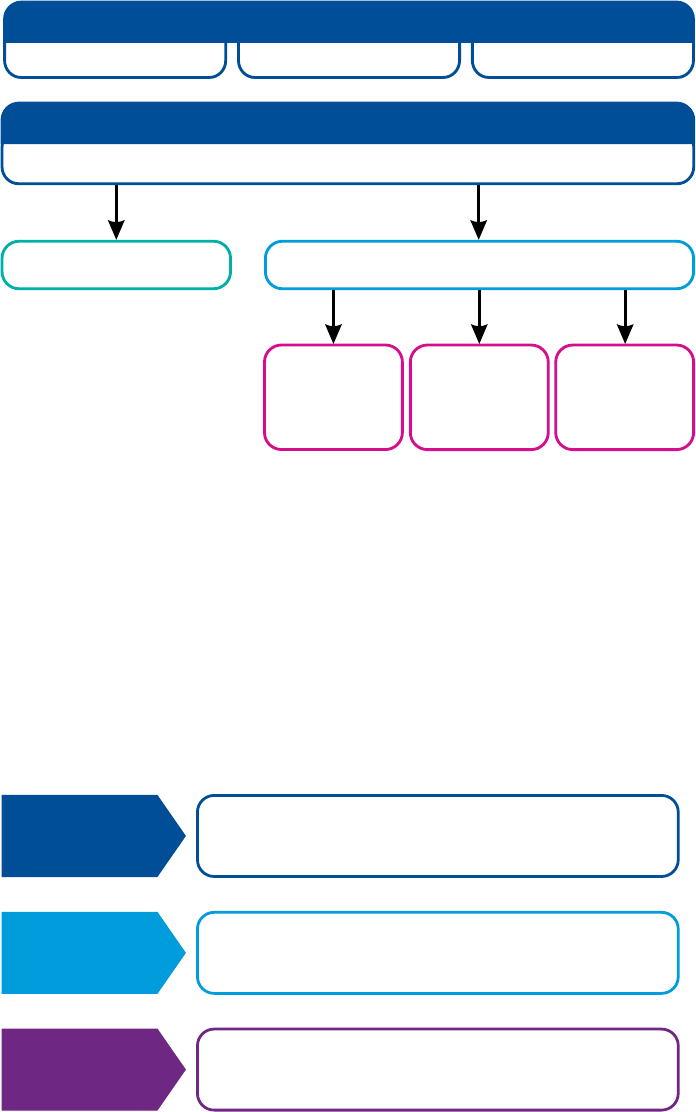

A contract with multiple leases may contain one or many separate lease

components.

Contract

Lease of sset AA

Separate lease component

for ssets A and BA

Separate lease

component for

sset CA

Lease of sset BA Lease of sset CA

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 7

2.2 Separate lease components

|

Example 3 – Multiple lease components: Separation criteria met

IFRS 16.B32

Lessee X enters into a 15-year lease for five floors of a building. The floors

are accessed via common lifts and stairs, but each floor has separate access

controls. Each floor is equipped with the necessary facilities (e.g. wash

rooms) to allow it to be used separately. X can sub-lease each floor without

significant work.

X concludes that the right to use each individual floor is a separate lease

component because:

–

–

X can benefit from the use of an individual floor on its own; and

the use of an individual floor is neither dependent on nor highly inter-related

with the use of other floors in the building. X can control access to each

individual floor separately

. In addition, each floor can be sub-leased without

significant work.

Example 4 – Multiple lease components in a master lease

agreement: Separation criteria met

Lessee C enters into a master lease agreement (MLA) with Lessor E to lease

30 vehicles for a fixed monthly payment of 5,000 per vehicle for a total term of

five years from delivery of the first vehicle.

C takes delivery of the 30 vehicles immediately. C concludes that the contract

contains 30 separate lease components, because:

–

–

C can benefit from using each vehicle on its own; and

each vehicle is independent of the other vehicles in the contract.

Example 5 – Multiple lease components: Land and building:

Separation criteria not met

IFRS 16.B32

Lessee T leases a single-storey industrial building from Lessor Q for five years.

T has exclusive use of the property, which includes a driveway. In addition to the

explicit lease of the building, there is an implied lease of the underlying land.

T concludes that there is a single lease component in the contract because:

–

–

it cannot derive any benefit from using the land without the building; and

the assets (i.e. building, driveway and land under the building) are highly

dependent on each other.

In this scenario,

T recognises a single lease liability with a corresponding right-

of-use asset.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

8 | Lease components

However, if the contract included the right to use an adjacent piece of land that T

could use for a number of different purposes (e.g. to redevelop into a garden or

a car park), then there might be multiple separate lease components – one for

the building, driveway and underlying land and another for the adjacent land.

Additional considerations may apply to Q’s assessment of whether to account

for the land and building elements separately – see Section 2.3.

Example 6 – Single lease component: Turbine plant: Separation

criteria not met

IFRS 16.B32

Lessor G leases a gas-fired turbine plant to Lessee P for 10 years to produce

electricity. The plant consists of the turbine housed within a building together

with the land on which the building sits. The building was designed specifically

to house the turbine, has a similar economic life to the turbine of approximately

15 years and has no alternative use.

G and P assess whether the lease of the turbine includes separate lease

components. The rights to use the turbine, the building and the land are highly

inter-related because each is an input into a combined item contracted for by P –

i.e. the right to use a gas-fired turbine plant that can produce electricity.

Therefore, G and P conclude that the contract contains only one lease

component.

Is identifying lease components under the new standard

consistent with identifying a performance obligation under

IFRS15?

IFRS 16.BC134

Yes, in broad terms. Identifying separate lease components in a lease contract

under IFRS 16 is similar to identifying performance obligations in a revenue

contract under IFRS 15.

Under both standards, a company determines whether a customer or a lessee

is contracting for a number of separate deliverables or for one deliverable.

Therefore, IFRS 16’s requirements on separating lease components are similar

to those in IFRS 15 on the identification of performance obligations.

However, IFRS 16 does not simply cross-refer to IFRS 15. Instead, it contains

guidance that is similar to, but less extensive than, that in IFRS 15. In addition,

IFRS 16 contains additional guidance for lessors on separation of the land and

building elements of a lease of real estate (see Section 2.3). In theory, different

conclusions could be reached under IFRS 15 and IFRS 16.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 9

2.2 Separate lease components

|

How can we interpret ’readily available’ when applying the first

criterion?

IFRS 15.27(a), 28

The first criterion for considering whether a right to use an asset is a separate

lease component is based on the ‘capable of being distinct’ test in IFRS 15. This

test is based on the characteristics of the underlying asset itself.

IFRS 16.B32

Resources are considered ‘readily available’ when they are sold or leased

separately by the lessor or other suppliers, or when the lessee has already

obtained them from the lessor or from other transactions or events.

The fact that the lessor or other companies regularly lease an asset separately

indicates that a customer can benefit from the lease of that asset on its own or

with other readily available resources.

For a discussion of identifying a performance obligation in a revenue contract,

see Section 2.1 of our IFRS 15 handbook – Revenue.

How can we interpret ’highly dependent or highly inter-related’

when applying the second criterion?

IFRS 15.27(b), 29(c)

The second criterion is based on part of the ‘distinct in the context of the

contract’ test in IFRS 15.

IFRS 16.B32

An asset might be highly dependent on, or highly inter-related with, the other

assets if the lessee could not lease the asset without significantly affecting its

rights to use other assets in the contract.

IFRS 15 provides an example of when two or more goods or services are

‘significantly affected by each other’. It states that this would be the case

when the company would not be able to fulfil its promise to the customer by

transferring each of the goods or services independently – i.e. the fulfilment of

each promise depends on the other.

For a discussion of identifying a performance obligation in IFRS 15, see

Section 2.1 of our IFRS 15 handbook – Revenue.

Does the identification of separate lease components always

affect the accounting outcome?

IFRS 16.12

No. In some circumstances, identifying a separate lease component will not

affect the lease accounting. In Example 3, the right to use each individual floor in

the building is identified as a separate lease component. However, accounting

for the right to use each of the five floors separately may be the same as

accounting for the five floors together. That is, the aggregate lease liability and

right-of-use asset, and the income statement effects would be the same.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

10 | Lease components

IFRS 16.B58

However, there may be circumstances in which this would not be the case. For

example, if Lessee X were to sub-lease one of the floors under a finance lease,

then it would derecognise the right-of-use asset relating to that floor. This would

require it to allocate the total consideration in the lease to each separate lease

component as described in Chapter 4.

Does pricing affect separating components?

No. Pricing is not considered when assessing whether the right to use an

underlying asset is identified as a separate lease component in a contract

involving multiple leases.

IFRS 16.B32

The separation criteria relate to the benefits from the right to use the asset

either on its own or together with other resources that are readily available, and

the relationship between the asset and the other assets for which the lessee

has a right of use in the contract – i.e. the asset is neither highly dependent on,

nor highly inter-related with, the other assets in the contract.

IFRS 16.B2

This is different from the contract combination test. When determining whether

two or more contracts are combined, the price interdependency is one criterion

to consider – if the amount of consideration to be paid in one contract depends

on the price or performance of the other contract, then the contracts are

combined as a single contract.

2.3 Lessors – Additional considerations for land

and buildings

IFRS 16.12, B53 The general guidance on identifying separate lease components is the same for

lessees and lessors. A lessor then classifies each lease component as a finance

or an operating lease, based on the extent to which the lease transfers the risks

and rewards incidental to ownership of the underlying assets (this guidance is not

relevant to lessees).

IFRS 16.B55, B57 When a lease includes both land and building elements, the lessor assesses the

classification of each element separately, unless the value of the land at inception

of the lease is deemed immaterial. In this case, the lessor may treat the land and

building as a single unit to classify it as either a finance or an operating lease,

applying the criteria in the new standard.

If separating the land element would have no effect on the lease classification,

then the lessor does not need to separate it because the accounting impact

would be insignificant. However, if the land and building elements are classified

differently – e.g. operating lease for the land and finance lease for the building –

then the lessor accounts for the two elements separately.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 11

2.3 Lessors – Additional considerations for land and buildings

|

IFRS 16.B56

When accounting for the land and building separately, the lessor allocates lease

payments between the two elements in proportion to the relative fair values of the

leasehold interests in the land and building elements at the date of lease inception.

This is different from the general allocation requirements – see Section 4.3.

IFRS 16.B56–B57 If the lease payments cannot be allocated reliably between the two elements, then

the entire lease is classified as a finance lease, unless both elements are clearly

operating leases.

IFRS 16.B32, B55–B57 When a lease contract contains both land and building elements, a lessor

considers the specific guidance described above, notwithstanding the fact that the

land and building might be highly interdependent and highly inter-related.

Example 7A – Classification of land and building: No separation

IFRS 16.61–63, B32, B55

Lessor Q leases a single-storey industrial building to Lessee T for five years.

T has exclusive use of the property, which includes a driveway. In addition to the

explicit lease of the building, there is an implied lease of the underlying land.

T and Q conclude that there is only one separate lease component in the

contract because:

–

–

T cannot derive any benefit from using the land without the building; and

the assets (i.e. building, driveway and land under the building) are highly

dependent on each other.

Ho

wever, as the lessor, Q is required to assess the classification of the land and

building elements separately. Q concludes that both land and building elements

are clearly operating leases. This is because Q does not transfer substantially all

of the risks and rewards incidental to ownership of either the land or building.

Therefore, separating the land and building elements would have no effect on

lease classification and would be insignificant from an accounting perspective.

Q classifies the entire lease as an operating lease.

Example 7B – Classification of land and building: Separation

required

IFRS 16.61–63, B55–B56

Modifying Example 7A, Lessor Q leases the building to Lessee T for 30 years.

The remaining economic life of the building on lease commencement is

expected to be 30 years.

T and Q conclude that there is only one separate lease component in the

contract.

Q assesses the classification of the land and building elements separately. Q

concludes that:

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

12 | Lease components

–

–

the land element is classified as an operating lease; but

the building element is classified as a finance lease, because the lease term

is for the major part of the economic life of the building.

Therefore, Q accounts for the land and building elements separately. To do this,

Q allocates the lease payments between the land and building elements in

proportion to the relative fair values of their respective leasehold interests.

Why does the standard include additional guidance on separating

land and building leases for lessors?

IFRS 16.B55, BC58

This guidance is brought forward from IAS

®

17 Leases to minimise changes

to lessor accounting. However, it is inconsistent with the general guidance

on separating components in a number of respects. For example, it requires

separate classification of land and building elements even when they would be

a single lease component. In addition, it requires lease payments to be allocated

based on relative fair values of the leasehold interests, rather than using the

principles in IFRS 15 that lessors are required to apply in other cases.

How small does the relative value of the land element need to be

in relation to the total value of the lease to avoid separation?

IFRS 16.BCZ250

The test here is whether the value of the land element at inception of the lease

is deemed immaterial. There is no bright line test – e.g. no specific percentage

threshold.

Generally, materiality as a concept is applied at the level of the financial

statements. However, this test – which is brought forward from IAS 17 –

typically considers the significance of the land element in relation to the lease,

not the financial statements as a whole.

Why does the lessor allocate the lease payments between the

land and building components based on the relative fair values of

the respective leasehold interests?

IFRS 16.B56, BCZ245–BCZ247

An allocation based on the relative fair values of the land and building elements

– rather than based on the relative fair values of the respective leasehold

interests in the land and building elements – is not generally appropriate

because the land often has an indefinite economic life and is likely to maintain

its value beyond the lease term. Therefore, the lessor would not normally need

compensation for ‘using up’ the land. In contrast, the future economic benefits

of a building are likely to be ‘used up’ to some extent over the lease term (which

is reflected via depreciation).

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 13

2.3 Lessors – Additional considerations for land and buildings

|

Therefore, when allocating the lease payments between the land and the

building elements, it is reasonable to assume that the lease payments relating

to the:

–

–

building element (depreciable asset) are set at a level that enables the lessor

not only to make a return on its initial investment, but also to recover the part

of the value of the building ‘used up’ over the lease term; and

land element (non-depreciable asset) (assuming a residual value that equals

its value at inception of the lease) are set at a level that enables the lessor to

make only a return on the initial investment.

Does an intermediate lessor that leases and sub-leases land and a

building classify the land element separately?

IFRS 16.B55, B57

As mentioned above, when a lease includes both land and building elements,

the lessor assesses the classification of each element separately, unless the

value of the land element at inception of the lease is deemed immaterial. When

determining whether the land element is an operating or a finance lease, an

important factor is that the land normally has an indefinite economic life.

IFRS 16.B58

An issue arises when a company leases land and buildings under a head lease

and sub-leases them as an intermediate lessor. In this case, the company

classifies the sub-lease with reference to the right-of-use asset arising from the

head lease. Therefore, the underlying asset for the land element of the sub-

lease does not have an indefinite economic life.

For example, if the head lease is for 20 years, which is similar to the estimated

useful life of the building, then the intermediate lessor does not separate the

land element from the building element to classify the sub-lease. However, if

the head lease for the land is for 999 years, then the intermediate lessor would

separate the land element when assessing classification.

2.3.1 Multi-tenant building

As mentioned in Section 2.3 above, if a lease of a building (or space in a multi-

tenant property) includes a land lease element, then that element is accounted

for separately by the lessor unless it is deemed to be immaterial or separation

would have no effect on the lease classification. Consequently, in such a lease the

lessor determines:

– whether the lessee obtains a right to use the land on which the building is

located; and if so

– whether the accounting for that right of use is immaterial or the classification

for both components would differ.

Determining whether a lease of a building (or space in a multi-tenant property)

includes a right to use the underlying land includes determining:

– whether the land represents an identified asset; and if so

– whether the lessee has the right to control its use.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

14 | Lease components

The evaluation will depend on property law in the relevant jurisdiction. However, it

will often differ for leases of single-tenant properties and leases of space in multi-

tenant properties. Although leases of single-tenant properties will generally include

a lease of the underlying land, leases of a space in multi-tenant properties often

will not.

Does a lessor of a multi-tenant building separate land and

building lease elements?

IFRS 16.B55

Generally, no. When a lessor owns a high-rise apartment building and leases

apartments to individual tenants, the lessor first needs to determine whether

there is a lease of the underlying land. If there is not, then the lessor does not

need to evaluate the separation criteria.

In this case, the entire underlying land is an identified asset. Each tenant has

only shared use of the land – i.e. no tenant has a right of use over a physically

distinct portion of the underlying land.

This is similar to the conclusion under IFRS 15 that in a sale of an apartment in a

multi-tenant building, the promise to transfer the apartment and the related land

can be a single performance obligation.

In contrast, a lease component may exist for the land if the lessee is leasing

substantially all of the building. In this case, the entire underlying land is likely

to be a single, identified asset and the lessee may have the right to control its

use. If that is the case, then the lessor is required to account for it as a separate

lease component unless it is immaterial or both components (i.e. the land and

the building leases) would have the same classification.

2.4 Portfolio approach

IFRS 16.B1 The new standard applies to individual lease components. However, as a

practical expedient a company may account for a portfolio of leases with similar

characteristics together if it reasonably expects that the effects of doing so would

not differ materially from accounting for each lease component individually.

Under the portfolio approach, the estimates and assumptions used to account for

leases reflect the size and composition of the portfolio – e.g. the discount rate or

lease term would be determined at the portfolio level, instead of at the individual

asset level.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Identifying separate lease components | 15

2.4 Portfolio approach

|

Example 8 – Applying the portfolio approach to leases of vehicles

IFRS 16.B1, Ex11

Lessee P enters into 50 individual lease contracts for similar cars during the

first quarter of the year. The leases have terms of two years and commence

on different dates within the same quarter. The annual lease payments are

between 5,000 and 6,000 for each car.

A separate lease exists for each car and is accounted for separately under

the new standard. Because the terms and conditions are similar for the lease

contracts, including similar start and end dates, and there is a narrow range

of fair values for the cars, P reasonably expects that the effect of applying the

new standard to these 50 leases as a portfolio will not differ materially from

applying it individually to each lease. Therefore, P applies the portfolio approach

to determine a single discount rate for these 50 leases.

P uses its incremental borrowing rate because it is unable to determine

the rate implicit in the leases. It determines this using the interest rate that

it would pay for a secured loan in the amount of the lease payments for a

representative lease in the portfolio (i.e. an amount between 5,000 and 6,000)

for a representative lease term.

How does the portfolio approach affect lease accounting?

IFRS 16.B1, BC82–BC83

Applying the portfolio approach to a group of lease contracts does not change

the company’s financial statements materially. However, this approach can

reduce the complexity and cost of accounting, especially for companies

with large groups of leases for similar assets. For example, establishing a

single discount rate for 50 leases in a portfolio will reduce the costs of lease

accounting compared with determining discount rates for each of 50 lease

contracts.

How does a company determine ‘similar characteristics’ when

applying the portfolio approach?

IFRS 16.BC82–BC83, Ex11, 15.BC69–BC70

The portfolio approach under the new standard is intended to be similar to that

under IFRS 15. Under IFRS 15, a company is not expected to evaluate each

outcome quantitatively, but applies judgement when selecting the size and

composition of the portfolio.

To apply the portfolio approach to a group of lease contracts, a company takes a

reasonable approach to determine the portfolio. The characteristics of the leases

to consider will include, for example, type or value of underlying assets, terms

and conditions of the contract, commencement date and lease term.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

16 | Lease components

3 Identifying non-lease

components

The new standard does not apply to non-lease components –

other standards apply.

3.1 Non-lease components

IFRS 16.12, 15 A lease contract often includes non-lease components. For example, a car lease

may include a maintenance or servicing component. A lessor always accounts

for non-lease components separately from the lease components. A lessee also

accounts for lease and non-lease components separately, unless it elects, as a

practical expedient, to account for a separate lease component and associated

non-lease components together as a single lease component – see Section 3.2.

IFRS 16.B33 Only activities or costs that transfer a good or service to the lessee are identified

as non-lease components. Amounts payable for activities and costs that do not

transfer a good or service are part of the total consideration and are allocated to

the lease and non-lease components identified in the contract. Common examples

of activities (or costs of the lessor) that do not transfer a good or service to the

lessee include the lessee’s payments for administrative tasks, insurance costs and

property taxes.

Right

to use an office

building

Cleaning and

maintenance services

Property taxes

and insurance

Lease component

Non-lease components Not a component

Accounted for

separately

Accounted for

separately

Not accounted for

separately

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Identifying non-lease components | 17

3.1 Non-lease components

|

Example 9 – Non-lease component: Common area maintenance

Lessee L enters into a three-year lease of an apartment. The apartment is in a

multi-tenant building that includes shared facilities – e.g. a swimming pool and

garden.

In addition to the monthly lease payments, the contract includes an additional

fee of 2,000 per quarter for the upkeep of the communal areas, maintenance

and security – i.e. common area maintenance (CAM). This fee does not cover

costs for non-routine and ‘major’ maintenance, which are billed to tenants

separately.

At commencement, the timing and extent of the landlord’s performance of

CAM is unknown (i.e. because it’s difficult to predict how many repairs will

be needed). However, the landlord has committed to keep the building and

common areas well maintained.

L determines that the CAM is a non-lease component because it transfers a

good or service to L other than the right to use the apartment – i.e. L receives a

service that it would otherwise pay for separately (e.g. for plumbing repairs). L

has not elected to apply the practical expedient to combine lease and non-lease

components. Therefore, L allocates the contract consideration to the lease

component and the non-lease component (CAM services). L accounts for the

lease component under the new standard; it expenses the amount allocated to

CAM as it is incurred.

Are CAM services a non-lease component?

IFRS 16.Ex12

Yes. It is common in a real estate lease for the lessor to provide CAM –

e.g. cleaning services, common area repairs or maintenance of a central

heating plant.

It appears that CAM services are generally a separate non-lease component(s)

because they transfer a service to a lessee that is separate from the right to

use the underlying asset. Therefore, they are accounted for separately from the

lease components, under other applicable standards. This applies to the lessor

and, unless it elects the non-separation practical expedient, to the lessee.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

18 | Lease components

Are property taxes part of the lease payments?

It depends. Real estate is often subject to property taxes, calculated as an

assessed value of the property multiplied by a tax rate. Depending on the

jurisdiction, the legal obligation to pay the property tax is either levied on the

property owner or on the occupier.

Lessee accounting for property taxes

This distinction is important for tenants to determine how to account for taxes

levied on the leased properties.

It appears that the lessee’s accounting for property tax is driven by the identity

of the statutory obligor. The identity of the party that makes the cash payment

to the tax authority is less relevant.

Who has the statutory obligation to pay property tax?

Lessor Lessee

If the lessor has the statutory

obligation to pay the property taxes,

but the lease agreement requires

them to be reimbursed, or paid, by

the lessee, then we believe that

the lessee should account for the

property taxes as part of the total

consideration that is allocated to

the separately identified lease

and non-lease components of the

contract. If the property taxes are

determined as a percentage of an

assessed value of the property,

then reimbursements thereof are

typically variable payments that do

not depend on an index or rate.

If the lessee has the statutory

obligation to pay the property taxes,

then we believe that the lessee

should account for the property

taxes as levies under IFRIC

®

21

Levies.

In some jurisdictions, the lessor and the lessee may be jointly liable for the

property taxes – i.e. both parties are equally liable to pay the full amount.

This may be the case if:

–

–

joint liability is specified by law; or

liability is placed initially on the lessor but, in the event of non-payment,

there are legal mechanisms in place that allow the tax authority to demand

payment from the lessee.

In this case, we believe that the lessee should account for the property taxes in

the same way as it would if it were solely liable for them – i.e. under IFRIC 21.

This is because they are considered to be a tax that is levied on the lessee and

are not a lease payment.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Identifying non-lease components | 19

3.1 Non-lease components

|

Lessor accounting for property taxes

When the lessor has a statutory obligation to pay the property taxes, the lessor

accounts for the property taxes as levies under IFRIC 21. The lessor accounts for

the reimbursement from the lessee as a part of the total consideration.

If a lessee reimburses a lessor’s general insurance costs, then is

this a non-lease component?

Generally, no. In practice, a lessor may obtain an insurance policy to cover the

damages to the underlying asset and a lessee reimburses the lessor’s insurance

costs during the lease term. The payment could be identified separately and

determined based on the lessor’s actual costs, or included in a fixed, gross

payment to the lessor.

In both cases, the insurance does not represent a service provided by the

lessor to the lessee and therefore it is not a separate component. The payment

is included in the consideration of the contract, which is allocated to the

components.

Is payment for value-added taxes included in the lease payments?

Generally, no. In many jurisdictions, a value-added tax (VAT), also referred to as

a ‘goods and services tax’ (GST), is charged on goods and services at the point

of sale. This may include leases. The specific rules for calculating and collecting

VAT may vary in different jurisdictions; however, the general principles are

typically as follows.

–

–

–

A seller charges VAT to the buyer, collects the VAT and then pays it to the

government.

If the bu

yer is not the end user and the good or service is purchased as a cost

to its business, then it can generally recover the VAT paid by deducting it from

the amounts that it remits to the government.

In some circumst

ances, the buyer cannot recover the VAT paid, either

because the goods or services do not qualify or because of the buyer’s

status. For example, in some countries banks and insurers are not eligible for

VAT refunds. In this case, the VAT is (partially or fully) irrecoverable.

It appears that if VAT is a tax that is levied on the lessee and collected by

the lessor, which is acting as an agent for the tax authority, then the VAT is

not a lease payment or a non-lease component regardless of whether it is

recoverable or non-recoverable. This is because the payment is not made in

exchange for the right to use an underlying asset or a good or a service provided

to the lessee.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

20 | Lease components

Instead, we believe that a lessee should account for this VAT as a levy under

IFRIC 21, even if it elects not to separate lease and non-lease components.

This means that a lessee should identify the obligating event for the VAT

payment under applicable laws and regulations. For example, if the obligating

event is the issue of each periodic invoice by the lessor, then the lessee should

recognise a liability for each VAT payment on each invoice date, not at lease

commencement. The obligating event for VAT should be assessed according to

the requirements of applicable legislation in each case.

3.2 Practical expedient for lessees – Combining

lease and non-lease components

IFRS 16.15 As a practical expedient, a lessee may elect, by class of underlying asset,

to combine each separate lease component and any associated non-lease

components and account for them as a single lease component. This does not

apply to embedded derivatives that are separated from the host contract in

accordance with IFRS 9 Financial Instruments.

Example 10 – Applying the practical expedient to combine lease

and non-lease components

IFRS 16.15, 38(b)

Lessee B enters into a five-year lease of an office building. The lease payments

are 10,000 per year and the contract includes an additional water charge

calculated as 0.005 per litre consumed. Payments are due at the end of the year.

B concludes that the water charge gives rise to a non-lease component in the

contract and elects to apply the practical expedient to combine lease and non-

lease components.

At the commencement date, B measures the lease liability as the present value

of the fixed lease payments (i.e. five annual payments of 10,000). Although B

has elected to apply the practical expedient to combine non-lease components

(i.e. water use) with the lease component, B excludes the water charges from

its lease liability because they are variable payments that depend on usage. That

is, the nature of the costs does not become fixed just because B has elected not

to separate them from the fixed lease payments. B recognises the payments for

water – as a variable lease payment

– in profit or loss when they are incurred.

In contrast, if B does not elect to apply the practical expedient to combine lease

and non-lease components, then it recognises the consideration allocated to the

water use – as an operating expense – in profit or loss as it is incurred.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Identifying non-lease components | 21

3.2 Practical expedient for lessees – Combining lease and non-lease components

|

What are the consequences of applying the practical expedient?

Applying the practical expedient for lessees not to separate non-lease

components from lease components has the potential to reduce cost and

complexity in some cases. However, lessees will also need to consider the

accounting consequences of applying it.

Some lessees may find the balance sheet consequences unattractive. Using

this practical expedient may result in recognising a liability for the service

component of the contract, which would otherwise remain off-balance sheet

until the landlord performs.

At the same time, using the practical expedient will impact the presentation in

the statement of profit or loss, with consequential impacts on key ratios.

For example, in a real estate lease the lessor may provide CAM to the tenants.

If the CAM is accounted for as a non-lease component, then the tenant will

typically recognise the consideration allocated to the CAM as an operating

expense as it is incurred. However, if the CAM is fixed or varies depending on an

index or rate and the tenant includes it in the lease payments, then it will not be

an operating expense. Instead, the company will effectively recognise additional

depreciation on the right-of-use asset and interest expense. In this example,

applying the practical expedient increases reported earnings before interest,

tax, depreciation and amortisation (EBITDA).

Can a lessee combine a lease component with significant non-

lease components?

IFRS 16.17, BC135(b)

Yes. The new standard does not prohibit a lessee from combining a small lease

component with significant associated non-lease components. However, it

is not acceptable for a lessee to combine a tiny lease with a large, unrelated

contract and artificially inflate EBITDA.

This practical expedient was provided to reduce cost and complexity for some

lessees, without creating significant issues of comparability. The International

Accounting Standards Board (the Board) expected that a lessee may not want to

adopt this practical expedient for contracts with significant service components,

because this would increase the lease liabilities for those contracts.

However, a lessee may want to apply this practical expedient for leases with

significant non-lease components for other reasons – e.g. to increase EBITDA.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

22 | Lease components

Can a lessor apply this practical expedient?

IFRS 16.17, BC135–BC136

No – there is no equivalent practical expedient for lessors. The Board considers

that a lessor, unlike a lessee, should have information about the value, or a

reasonable estimate, of each lease and non-lease component. This is because

it needs the information when pricing the contract. In addition, the requirement

to allocate the consideration in the contract by applying IFRS 15 ensures

consistency for companies that are both a lessor and a seller of goods or

services in the same contract.

Can a lessee choose to apply this exemption on an asset-by-asset

basis?

IFRS 16.15

No. The practical expedient of combining lease and associated non-lease

components can only be elected by class of underlying asset. Therefore, a

lessee is not allowed to apply it on an asset-by-asset basis.

For example, if a lessee elects to apply this practical expedient to an office

building lease, then the lessee applies the same accounting to all of the

associated non-lease components for other office building leases.

Can a lessee choose to combine only one non-lease component

when there are more than one?

IFRS 16.15

No. The lessee can elect, by class of underlying asset, not to separate non-lease

components from lease components, and to account for them as a single lease

component. Therefore, a lessee that elects to apply the practical expedient for

a class of underlying asset combines all non-lease components in the contract

that are associated with the lease.

For example, a lessee that elects to apply the practical expedient to office

building leases accounts for the lease component and all associated non-

lease components – e.g. CAM and security services provided under the same

contract – as a single lease.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Identifying non-lease components | 23

3.2 Practical expedient for lessees – Combining lease and non-lease components

|

Can a lessee combine a non-lease component that is not

associated with the lease component?

IFRS 16.15

No. A lessee can only combine those non-lease components that are associated

with the lease.

For example, a lessee enters into a contract to lease IT equipment, along with

maintenance for that leased IT equipment and for other IT equipment that it

owns.

If the lessee elects to apply the practical expedient, then it can combine the

maintenance service for the leased IT equipment with the lease of IT equipment

to account for it as a single lease. However, the maintenance of its own

equipment cannot be combined and is accounted for separately.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

24 | Lease components

4 Allocating the

consideration

Consideration is allocated based on relative prices.

4.1 Contract consideration

IFRS 16.A, 13, 17 The new standard requires both the lessee and lessor to allocate consideration to

the lease and non-lease components. The consideration includes all payments in

the contract – i.e. those that relate to lease and non-lease component(s), and other

payments that relate to items such as taxes, which are not separate components.

4.1.1 Timing of measurement of contract consideration

If different components of a contract commence at different dates, then a question

arises over the date(s) at which the contract consideration is measured. The

new standard requires the lessee and the lessor to measure the lease liability

on commencement of a lease. However, when the components are recognised

at different times, it is not clear how the lessee and lessor measure any

related amounts.

In the absence of guidance in the new standard, it appears that the lessee and

lessor should make a preliminary estimate of the consideration in the contract

when the first component commences and allocate it to the lease and non-lease

components using relative stand-alone prices. This will generally include, among

other things:

– measuring variable payments that depend on an index or a rate based on the

index or rate at that point in time;

– assessing whether a renewal option is reasonably certain to be exercised; and

– estimating any expected amounts to be paid under a residual value guarantee.

However, because the new standard requires measurement of lease payments

as at the commencement of the lease, it appears that the lessee and the lessor

true up the initial measurements and allocation of the consideration at the

commencement date.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Allocating the consideration | 25

4.1 Contract consideration

|

Example 11 – Master lease agreement: Minimum commitment and

different commencement dates; each additional right-of-use asset

priced at stand-alone price

Lessee C enters into an MLA with Lessor E to lease up to 50 vehicles for a fixed

monthly payment of 5,000 per vehicle for a total term of five years from delivery

of the first vehicle. The monthly payment per vehicle is the stand-alone price and

does not change depending on how many vehicles are delivered to C.

C is required to take delivery of 20 vehicles immediately and then a minimum of

10 additional vehicles from E by the end of Year 2.

The MLA creates enforceable

rights and obligations and is itself a contract, because it includes committed

delivery of a minimum of 30 vehicles.

When C takes delivery of any of the 10 mandated additional vehicles, there is

no lease modification (for details, see our publication Lease modifications). That

is, for draw-downs up to the minimum required quantity of 30 there is no lease

modification. For these vehicles, C applies the guidance in the new standard

on identifying separate lease components and allocating the consideration in

the contract to those components. C accounts for each vehicle lease from its

commencement date.

Therefore, although there is no lease modification resulting from drawing down

10 additional vehicles after taking delivery of the first 20, some measurement

and allocation complexities could arise if there were, for example, residual value

guarantees or if the monthly lease payments escalated during the lease term

based on an index or rate – e.g. the consumer price index (CPI).

Additional complications arise if the lease contains a number of lease

components but with different commencement dates and there is a price

inter-dependency (e.g. a volume discount) or other non-lease components (e.g.

maintenance services) exist in the contract.

As mentioned above, in the absence of guidance it appears that the lessee and

lessor should make a preliminary estimate of the consideration in the contract

when the first component commences and allocate it to the lease and non-lease

components using relative stand-alone prices.

However, if C takes delivery of more than 30 vehicles in total (the minimum

required), then as each additional vehicle is delivered this is a lease modification.

In this case, the scope of the lease is increased because C receives the right

to use another underlying asset and the consideration for the lease increases

by an amount that is commensurate with the stand-alone price for the increase

in scope. Therefore, C accounts for the right to use each additional vehicle as a

new lease.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

26 | Lease components

Example 12 – Non-lease component provided before

commencement date

Lessor R agrees to lease a piece of new IT equipment to Lessee L and provide

maintenance services for L’s existing IT equipment. At the inception date, the

leased IT equipment is on backorder and is expected to be available two months

later. However, R agrees to start providing maintenance services on the existing

equipment immediately.

The lease of IT equipment is for five years. The annual payment for the lease and

maintenance services is fixed, payable from the commencement date of the

lease. L also guarantees the residual value of the equipment.

L and R identify two components in the contract:

– a lease of IT equipment; and

– maintenance services (a non-lease component).

L begins recognising expense, and income, for the maintenance services that

have been provided before the commencement date. It appears that at the

inception date, R and L should make a preliminary estimate of the consideration

in the contract – i.e. estimate the amount payable under the residual

value guarantee.

However, the new standard requires measurement of the consideration at the

lease commencement date. At that date, we believe that R and L should also

make adjustments to the initial estimate of the consideration – i.e. estimate the

amount payable under the residual value guarantee.

4.2 Allocation of consideration

IFRS 16.13, 17 The consideration in the contract is allocated to each lease and non-lease

component.

The allocation of the consideration is a two-step process.

1. Determine the stand-alone price for each component.

2. Allocate the consideration.

The new standard is clear that payments for activities and costs that do not

transfer a good or service to the lessee do not give rise to a component (see

Section 3.1). The payments are included in the consideration that is allocated to

the separate lease and non-lease components in the contract.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Allocating the consideration | 27

4.3 Lessor allocation

|

Contract

Lease

components

Non-lease

components

NOT a component

Allocate contract consideration

Activities that do not transfer a good

amounts payable for

these items are part of the total

consideration that is allocated to the

lease and non-lease components

or service –

The new standard requires different approaches for the lessor and the lessee.

Lessor Lessee

IFRS 16.13–14, 17

When there is

an observable

stand-alone

price for each

component

Allocate the consideration

following the IFRS 15

approach – i.e. on a

relative stand-alone

selling price basis (see

Section4.3).

Allocate the consideration

based on the relative

stand-alone price of

components (see

Section4.4)

When there is

no observable

stand-alone price

for some or all

components

Allocate the consideration

based on the stand-alone

selling price, estimated

using observable

information (see 4.4.1)

4.3 Lessor allocation

IFRS 16.17, 15.74–77 A lessor allocates consideration in a contract to the separate lease and non-lease

components by applying IFRS 15. Under IFRS 15, consideration is allocated on

a relative stand-alone selling price basis. Stand-alone selling price is determined

at inception of the contract and is the price at which a company would sell a

promised good or service separately to a customer. It is best evidenced by the

observable price of the same good or service when the company (lessor) sells (or

leases) that good or service separately.

IFRS 15.81–86 IFRS 15 also has detailed guidance on the allocation of variable consideration or

discounts to one or more components in the contract. See Section 4.2 of our

IFRS15 handbook – Revenue.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

28 | Lease components

IFRS 15.79

Adjusted

market

assessment

approach

Expected cost

plus a margin

approach

Residual

approach

(only in limited

circumstances)

Allocate based on relative stand-alone selling prices

Performance obligation 1

Performance obligation 2Performance obligation 3

Determine stand-alone selling prices

Use the observable price Estimate price

Is observable price available?an

Ye

sN

o

4.3.1 Estimating the stand-alone selling price

IFRS 15.78 A lessor considers all information that is reasonably available when estimating

a stand-alone selling price – e.g. market conditions, entity-specific factors and

information about the customer or class of customer. It also maximises the use

of observable inputs and applies consistent methods to estimate the stand-alone

selling price of other goods or services with similar characteristics.

IFRS 15.79 IFRS 15 does not preclude or prescribe any particular method for estimating the

stand-alone selling price for a good or service when observable prices are not

available, but describes the following estimation methods as possible approaches.

Adjusted market

assessment

approach

Expected cost

plus a margin

approach

Residual

approach (limited

circumstances)

Subtract the sum of the observable stand-alone selling

prices of other goods or services promised in the

contract from the total transaction price

Forecast the expected costs of satisfying a performance

obligation and then add an appropriate margin for that

good or service

Evaluate the market in which goods or services are sold

and estimate the price that customers in the market

would be willing to pay

IFRS 15.88 After contract inception, a lessor does not reallocate the transaction price to reflect

subsequent changes in stand-alone selling prices.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Allocating the consideration | 29

4.3 Lessor allocation

|

Using the residual approach to estimate stand-alone selling prices

IFRS 15.79(c) The residual approach is appropriate only if the stand-alone selling price of one

or more goods or services is highly variable or uncertain and observable stand-

alone selling prices can be established for the other goods or services promised in

the contract.

Selling price is… If…

Highly variable The lessor sells the same good or service to different

customers at or near the same time for a broad range

of prices

Uncertain

The lessor has not yet established the price for a good

or service and the good or service has not previously

been sold on a stand-alone basis

Under the residual approach, a lessor estimates the stand-alone selling price of

a good or service on the basis of the difference between the total transaction

price and the observable stand-alone selling prices of other goods or services in

the contract.

It appears that the total transaction price used in applying the residual approach

should include the estimated amount of any variable consideration before

applying the constraint (see Section 3.1 of our IFRS 15 handbook – Revenue). This

approach is consistent with the allocation objective because the estimated variable

consideration is the amount of consideration to which the company expects to

be entitled.

IFRS 15.80 If two or more goods or services in a contract have highly variable or uncertain

stand-alone selling prices, then a lessor may need to use a combination of

methods to estimate the stand-alone selling prices of the performance obligations

in the contract. For example, a lessor may use:

– the residual approach to estimate the aggregate stand-alone selling prices for all

of the promised goods or services with highly variable or uncertain stand-alone

selling prices; and then

– another technique to estimate the stand-alone selling prices of the individual

goods or services relative to the estimated aggregate stand-alone selling price

that was determined by the residual approach.

4.3.2 Allocate the consideration

IFRS 15.76, 81–86 At contract inception, the transaction price is generally allocated to each

performance obligation on the basis of relative stand-alone selling prices (see

Example 13). However, when specified criteria are met a discount or variable

consideration is allocated to one or more, but not all, of the performance

obligations in the contract (see Section 4.5).

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

30 | Lease components

IFRS 15.88–89 After initial allocation, changes in the transaction price are allocated to satisfied and

unsatisfied performance obligations on the same basis as at contract inception,

subject to certain limited exceptions. For a discussion of changes in a transaction

price as a result of a contract modification, see Section 8.2 of our IFRS 15

handbook – Revenue.

When a contract contains lease and non-lease components, the lessor allocates

consideration to the lease and non-lease components in accordance with IFRS 15.

However, if the contract contains a renewal option covering the lease and non-

lease components, then the lessor may determine that the contract period under

IFRS 15 differs from the lease term under IFRS 16. The lease term as determined

under IFRS 16 includes optional renewal periods over which the lessee is

reasonably certain to extend, whereas the contract term under IFRS 15 includes

periods during which the parties have presently enforceable rights and obligations.

In these cases, it appears that a company should allocate the consideration to

each component based on the lease term as determined under IFRS 16 (see

Example 14).

Example 13 – Lessor allocation of consideration: Observable and

estimated stand-alone selling prices

Lessor R leases a specialised machine for two years to Lessee L and provides

consulting services to help L use the machine effectively in its production

processes. The machine is not sold or leased separately by R and there are no

similar machines for sale or lease from other suppliers.

The consideration is 100,000 for the first year and 80,000 for the second year.

R priced the contract in this way assuming that it will provide more consulting

services in the first year.

R allocates the consideration using estimated stand-alone selling prices,

because it does not provide the machine or consulting services separately.

R estimates the stand-alone selling prices as follows.

–

–

There are no similar machines for lease by other suppliers to assess.

Consequently, R uses expected cost plus a margin to arrive at a stand-alone

selling price of 160,000 for the machine lease.

R uses a market-based assessment approach to arrive at a stand-alone price

of 40,000 for the consulting services based on similar services offered in the

marketplace.

On this basis, R allocates the consideration as follows.

Stand-alone

price Calculation Allocation

Machine lease 160,000 80% x 180,000 144,000

Consulting service 40,000 20% x 180,000 36,000

200,000 180,000

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Allocating the consideration | 31

4.3 Lessor allocation

|

Example 14 – Lessor allocation to lease and non-lease components

based on the lease term

Lessor R leases a bulldozer to Lessee T. Under the arrangement, R also provides

maintenance services for the bulldozer for the entire lease term.

The original contract term is five years, with a renewal option for another

two years. Annual payments, including maintenance, are determined at 160

for the initial five years. For the extension period, annual payments including

maintenance are reduced to 150. Therefore, if the contract runs for five years

then the total consideration will be 800, whereas if the contract runs for

seven years then the total consideration will be 1,100.

The stand-alone price of the lease without maintenance is estimated at 120 per

year, and the stand-alone price for the maintenance is 50 per year.

At the commencement date, R and T conclude that the lease term is seven

years, because it is reasonably certain that T will exercise the renewal option.

If the contract were wholly accounted for under IFRS 15, then the contract term

would be five years because this is the period for which the two parties are

contractually committed. The lease is classified as an operating lease.

We believe that R should allocate the consideration to the lease component and

maintenance services based on the lease term as determined under IFRS 16

– i.e. seven years. Therefore, R allocates the total consideration based on

seven years (1,100) to the lease and non-lease components as set out below.

Stand-alone

price % Allocation

Bulldozer lease 120 x 7 = 840 70.59% 776

Maintenance 50 x 7 = 350

29.41%

324

1,190 1,100

Does the lessor need to allocate consideration when the

allocation does not have an impact on the income?

IFRS 16.90, 15.114, B87–B89

Yes, the lessor allocates the consideration to each of the lease and non-lease

components, even if there is no impact on the profile of income recognised. This

is necessary for presentation and disclosure purposes – i.e. the new standard

requires a lessor to disclose lease income. IFRS 15 also requires a company to

present and disclose revenue from contracts with customers separately.

For example, when the lease is classified as an operating lease and the non-

lease component is a service satisfied over time using a time-based measure,

the income from both the lease and non-lease components is recognised

over the period: the allocation does not impact the income recognised during

the period.

© 2019 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

32 | Lease components

4.4 Lessee allocation

IFRS 16.13–14 If a contract contains a lease component and one or more additional lease or

non-lease components, then the lessee allocates the consideration in the contract

to each component on the basis of: